The ATG Blog

An Overview of What to Expect on Closing Day

Closing day is the pinnacle of a real estate transaction, the moment everyone’s hard work has been leading to: The successful transfer of ownership of a property. Whether you are purchasing your first home or selling one of your investment properties, understanding what to expect on this day can help alleviate stress. Rest assured, the lender (if applicable), title company, and real estate agents involved have been working diligently to handle all of the behind-the-scenes work in order to facilitate a smooth closing with no surprises.

Laying the Groundwork

By the time you gather at the closing table — usually at the title company’s office — several milestones have already occurred, setting the stage for a successful closing:

- If applicable, the buyer has secured financing and received a Closing Disclosure outlining the final financial details (loan terms, closing costs, etc.). Buyers must receive this at least three business days before closing.

- The title company has conducted a thorough title search to verify the property’s legal ownership and ensure it’s free of any outstanding liens, encumbrances, or claims. Based on the title search, the title company has prepared a title insurance policy to protect the buyer and the lender against future title defects.

- The buyer has likely completed a final walkthrough of the property and confirmed that any requested repairs have been completed. This is the final opportunity to confirm that the property is in the agreed-upon condition.

- Both buyer and seller, along with their respective agents, have confirmed the closing date and that all contingencies have been lifted.

ATG Announces Opening of Newest Office Location in Fayetteville, AR

Attorney’s Title Group, LLC, (“ATG”), a trusted provider of title and closing services in Arkansas, has announced that it is opening its newest office location in Fayetteville, Arkansas. Located at 104 N. East Avenue, Suite B, the location is in a shared space with the company’s affiliated firm, Wilson & Associates. The Fayetteville office will provide a comprehensive suite of real estate title and closing services to homebuyers, sellers, builders, investors, and real estate agents and lenders in Fayetteville and the surrounding areas. Kris Conant will be leading the closing operations at the Fayetteville office. Kris currently works in the company’s Rogers location along with Amy Renee Ellenbarger.

“Opening our Fayetteville location is an exciting milestone because it marks the continued expansion of ATG and our commitment to serve the growing real estate market in Northwest Arkansas,” said Robbie Wilson, co-managing partner of Attorney’s Title Group. “We are looking forward to being a part of the Fayetteville community and looking forward to building strong relationships with local real estate agents and lenders and residents.”

To celebrate the opening of its newest location, Attorney’s Title Group is hosting a grand opening event on Thursday, June 5th from 12:00-3:30 PM at the new Fayetteville office. The event will kick off at noon with an official ribbon cutting and will provide an opportunity for the community to meet the ATG team, see the new space, and enjoy refreshments.

more

Avoiding Boundary Disputes in Real Estate

Whether you're a real estate agent, a homebuyer, or a seller, knowing the details around avoiding boundary disputes is essential for a smooth property transaction. Boundary disputes can delay the selling or buying process, lead to costly legal issues, and cause stress to all parties involved. To help you avoid such pitfalls, here are straightforward steps to ensure there are no boundary disputes on the house you're looking to buy or sell.

Obtain a Title Search

The first and foremost step is to get a title search. A title search is an examination of public records to confirm a property's legal ownership and find any encumbrances or liens on the property. Importantly for boundary issues, a title search can sometimes reveal historical information or recorded documents that might hint at past boundary concerns.

Review the Property's Legal Description

Every property has a legal description that outlines its boundaries, far more accurately than its street address. The property deed, a legal document outlining ownership, should contain a detailed description of your land's boundaries or references to a recorded subdivision plat. Review the legal description in the property's deed or the title report. If there's any confusion or any part of it raises questions, consult a real estate attorney or a title company for clarity.

more

Home Sweet Home: Move-In Ready or Fixer-Upper - Which is Right for You?

The dream of homeownership comes with a pivotal question: Do you opt for a move-in-ready sanctuary or a fixer-upper brimming with potential? For first-time buyers and seasoned homeowners alike, this decision can feel overwhelming. It's a balance between immediate comfort and the opportunity to create a personalized space. Let's explore the advantages and disadvantages of each option to help you navigate this important choice.

Move-In Ready Homes: The Appeal of Instant Gratification

These homes, whether newly built or meticulously renovated, offer the allure of immediate occupancy with fewer projects on your to-do list.

- Predictable Budgeting: With renovations complete, you have a clearer picture of your upfront costs. If it’s a newer home with recently installed appliances and systems, you may be avoiding potential replacement costs. For example, you won't suddenly need to replace a dishwasher or HVAC system.

- Aesthetic Appeal: Modern finishes and updates may appeal to you, and will also contribute to the home's future marketability. Imagine coming home to a freshly painted home with new flooring and updated appliances.

- Convenience and Time Savings: Skip the construction chaos or the decision-making process that may come with a fixer-upper, and move right on in! This frees up valuable time and reduces stress during what can already be a stressful process.

Wishing Charles Ward the Best in His Retirement!

The below article was written by Jordan Winter, originally published in an internal company newsletter.

I officially met Charles Ward when I began working for Attorney’s Title Group in 2020. I was still supervising the title curative and post-sale departments for Wilson & Associates at the time, but ATG needed help, and I had some time. I had worked with Charles a few times before on post-sale files, but that was just through an email from time to time. Over our few prior interactions, though, I could tell Charles had boundless knowledge in real property title. When I began working full time at ATG in 2021, Charles trained me on their title processes. He always seemed to have the answer, and I appreciated his willingness to let me pick his brain on a title question. I knew Charles had worked at the firm a long time, but it wasn’t until I started working with him on a daily basis that I truly understood how lucky the firm was to have him and how lucky I was to learn from him. Now on the brink of retirement, I find it fitting to take a brief look back on Charles’ career and the 30 years he has dedicated to the W&A and ATG.

Charles is a Little Rock native and attended Hall High School (shout out to the class of 1973). His first jobs growing up were a local paper route and a bagger at a grocery store. I’m sure he hit the front porch every time and double-bagged like the best of them! After high school, he went on to Fayetteville where he graduated from the U of A in 1977. Graduating college in four years delighted his father, he said, as he likely wasn’t going to foot the bill for another year. After college, Charles wasn’t exactly sure what he wanted to do in life (like many of us), so he began working at a bank. He chose not to pursue a career in banking, however, and in 1981 he began law school at UALR, graduating in 1984. He served as a law clerk for Wilson & Associates during his last year of law school.

more

Don’t Let Neglect Cost You: The Importance of Home Maintenance

We all get busy. Life throws curveballs, and sometimes, the little things like home maintenance can fall by the wayside. When was the last time you truly inspected your roof? Or gave your HVAC system a thorough check-up? If you're drawing a blank, you're not alone.

However, regular home maintenance is crucial to not only retaining your home's value and avoiding costly repairs, but it’s also important in keeping it safe for you and your family. Let's explore why you should prioritize home maintenance and what inspections to add to your to-do list.

Why Home Maintenance Matters

Your home needs regular care and attention to remain at its best. There are a few key reasons why you should prioritize home maintenance.

- Prevent Expensive Disasters: Home maintenance means you're regularly inspecting your property. Routine inspections help identify and address minor issues before they escalate into major, expensive repairs. A leaky roof left unchecked can lead to more significant water damage, while a neglected HVAC system can skyrocket your energy bills or cause it to malfunction when you need it the most.

- Protect Your Investment: Your home is likely your most significant financial asset. Proper maintenance ensures you get the best possible return on your investment. A well-maintained home is more appealing to potential buyers and can significantly increase your property's resale value. It's a competitive market, with an increasing number of older homes for sale. To boost your property's appeal, keep it well-maintained.

- Enhance Your Family's Safety and Well-being: A well-maintained home is a safe home. Regular checks for potential hazards like fire risks (faulty electrical wiring, clogged chimneys), carbon monoxide leaks, and water damage protect your family, pets, and/or belongings.

Robbie Wilson Voted Among Little Rock's Best Lawyers 2024

Attorney's Title Group is proud to announce that Robbie Wilson was again voted as one of Little Rock’s Best Lawyers in the December 2024 edition of Soiree magazine. Robbie was recognized in the Commercial Real Estate category.

The Little Rock Best Lawyer list is composed of 113 individuals who are determined via a two-component voting system of peer review voting and voting by the readers of Little Rock Soiree and Arkansas Business magazines. The expertise of lawyers is used to determine who should be on the list, and readers votes and experiences with the lawyers determine how individual lawyers rank.

Congratulations to Robbie on this well-deserved achievement.

more

Six Overlooked Expenses to Plan for After Buying a House

Buying a house is an exciting milestone, but the journey doesn't end at closing. While you may have budgeted for the down payment and closing costs, new homeowners can face several other expenses that are often overlooked. Planning for these expenses can help you manage your finances better and enjoy your new home without stress.

1. Home Maintenance and Repairs

Home maintenance is an ongoing expense that many new homeowners underestimate. From routine tasks like regular lawn care and gutter cleaning to unexpected repairs like fixing a leaky roof or replacing a broken HVAC system, these costs can add up quickly. Setting aside a pre-determined amount (for example, 1%) of your home's purchase price annually for maintenance and repairs is wise. Some buyers opt in for additional options, such as a home warranty, as an added way to prepare for home repair expenses; however, that cost also needs to be factored into your planning. Don’t forget to consider future cosmetic updates or items such as furniture and housewares you may need.

2. Homeowners Insurance

Homeowners insurance is a necessary expense, but costs can vary widely depending on your location, the age of your home, and the coverage you choose. You may also need additional coverage for events like floods or earthquakes, which can significantly increase your insurance premiums. Also, this cost isn't fixed – there is some potential that it may rise annually.

more

The Power of Partnership: Attorney’s Title Group Values Everyone’s Role in Real Estate Transactions

At Attorney’s Title Group, we believe that every real estate transaction is a journey, and each individual involved plays a crucial role in its success. From real estate agents and mortgage lenders to home buyers and sellers, your partnership is essential to ensuring a smooth and efficient process. We're committed to fostering strong relationships with all of our partners and customers, recognizing the unique value that each brings to the table.

The Importance of Real Estate Agents

Real estate agents are the front-line professionals who guide clients through the complex world of buying and selling property. The expertise, knowledge, and dedication of a real estate agent are invaluable to buyers and sellers. We understand the importance of their role and strive to provide agents with the tools, resources, and support they need to succeed. By offering timely communication, efficient processing, and personalized service, we aim to make their job easier and more rewarding. Our goal is to ensure that the real estate agents we work with feel well represented before, during, and after each closing.

The Role of Mortgage Lenders

Mortgage lenders are the financial architects of real estate transactions, providing the necessary funding to make homeownership a reality. Their careful evaluation of loan applications and adherence to regulatory guidelines ensure the stability and security of the transaction. We value our partnerships with mortgage lenders and work closely with them to streamline the closing process and minimize delays for our mutual customers. By maintaining open lines of communication and providing timely updates, we help to protect their interests and ensure a smooth closing experience.

more

Attorney’s Title Group Announces New Closing Agent in Northwest Arkansas

ROGERS, AR (August 21, 2024) – Attorney’s Title Group, LLC, (“ATG”) has announced that it has hired Kris Conant as a closing agent in their Northwest Arkansas location.

Kris is an experienced real estate professional with a proven track record of success in the title and closing industry. Kris has honed her skills in managing complex transactions and delivering exceptional customer service.

“We’re very excited to welcome Kris on board. Her experience and knowledge will be invaluable as we continue to expand in the Northwest Arkansas area,” said Robbie Wilson, co-managing partner of Attorney’s Title Group.

In addition to implementing ATG’s high level of customer service and delivering exceptional title and closing services, Kris will be working closely with the ATG operations team to ensure that the client experience with Attorney’s Title Group is first rate. Prior to her time in the title industry, Kris worked for 10 years in customer service and retail management. Her background in customer service and retail management has equipped her with a deep understanding of client needs and a commitment to building lasting relationships.

more

What Does the “As-Is” Clause Mean in Real Estate?

As the name indicates, the “as-is” clause in a real estate transaction means a property is being sold in the current condition, as it exists, with any faults and defects. This brings with it some benefits but also some risks that must be considered.

The benefits to consider are usually pretty clear, some of them being:

- A reduced price: Since the buyer will be responsible for any repairs, an “as-is” property will typically be priced lower, and depending on circumstances, sellers may even still consider lower offers than the listing price.

- Expediency: An “as-is” property will likely require much less paperwork and negotiation time because the seller isn’t obligated to fix any problems beforehand. That means that the inspection would solely serve as an informational tool to understand the property’s condition, and the costs associated with any repairs.

While “as is” doesn’t always mean a home is in disrepair, the risks of buying an “as-is” property could be quite considerable, and they need to be considered before entering into any such contract.

- Hidden issues: The most common problem is, of course, the hidden issues that could come up with the property, including electrical issues, plumbing issues, roof leaks, mold problems, or even foundational cracks.

- While buying a home “as-is” doesn’t mean you’re giving up your legal rights as a buyer, depending on the state in which the property is located, there might be limited seller disclosure, which means the seller might not be obligated to disclose all known issues with the house. That means you could purchase a property with many more problems than you know. Again, this is dictated by state regulations so be sure to ask your real estate agent about the disclosure laws and what information you’re entitled to as the borrower.

- Problems with financing: “As-is” properties are sometimes more challenging to get mortgages for because there is an increased risk of major repairs. Most loan types will require that the property meets certain livability standards, known as “minimum property requirements.” That means you might need to put down a much larger down payment, pay cash, or secure a special loan program. This sometimes depends on the level of repairs needed. It’s important to discuss with your lender before taking any additional action.

- Resale issues: An “as is” property might be challenging to resell in the future, particularly if all the issues aren’t addressed when you purchase the property.

Protection Against Title Fraud

Real estate fraud is becoming an increasingly common way for criminals to steal someone’s property, and while it is less common than other types of fraud, title fraud is a form of real estate fraud that homeowners need to be aware of. Home title fraud is essentially the forging of a deed to transfer ownership of property away from the true owner in order to profit from the theft of the property.

The steps to commit title fraud, sometimes known as deed fraud, generally follow a similar pattern:

- Scammer identifies a property they want to acquire or that they deem as an easy target for committing title fraud (such as vacant properties).

- They forge any necessary real estate documentation, such as a deed, which transfers ownership to them, and have it filed on record with the county.

- The new “owner” either sells the property or takes out a home equity line of credit loan against the property. The true property owner may only discover they no longer own their property when they get a notice of the new mortgage or when a bank begins the process to foreclose on the property.

- The scammer may commit identity theft to steal a homeowner’s identity and transfer the deed to their name (meaning they fraudulently act as the homeowner and then transfer the property to themselves).

Attorney's Title Group voted as "Most Admired Title Company" in AMP Magazine

Arkansas Money & Politics ("AMP") released its 2024 "Most Admired Companies" list in which readers throughout Arkansas nominated companies in multiple business categories. The criteria used for nominations included financial soundness, bold innovation, brand awareness, quality of product, outstanding people, and social responsibility.

Attorney's Title Group is honored to have been selected as the "Most Admired Title Company" in Arkansas. This recognition is a testament to the dedication and hard work of our team, as well as the loyalty of our customers.

To learn more and see other companies listed, visit AMP online at the following link, or pick up the June 2024 edition of Arkansas Money & Politics.

https://armoneyandpolitics.com/amp-most-admired-companies-2024/

more

Attorney’s Title Group Announces Opening of Newest Office Location in North Little Rock

NORTH LITTLE ROCK, AR (May 7, 2024) – Attorney’s Title Group, LLC, (“ATG”) has announced that it is opening its newest office location in North Little Rock. The office is located at 5600 JFK Boulevard, Suite 3, and will be managed by Shirley Worthy.

Worthy began her career in real estate as a real estate agent in 2003. She became a licensed real estate broker in 2016, at which time she began instructing real estate courses. She has a wealth of real estate knowledge, and is also very familiar with North Little Rock, Sherwood, Jacksonville, and surrounding communities.

“We are very excited to join the North Little Rock community. Between Shirley’s background in real estate and her involvement with different organizations in the area, we are confident that this location will thrive,” said Robbie Wilson, co-managing partner of Attorney’s Title Group.

Attorney’s Title Group also offers remote, concierge closings at real estate offices, banks, and businesses. The company is headquartered in West Little Rock, with additional offices in downtown Little Rock, Conway, and Rogers. Attorney’s Title Group welcomes all businesses and homeowners in the North Little Rock area to experience the “Attorney’s Title Group Difference.”

more

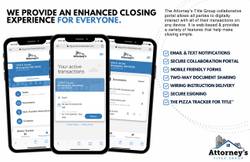

Introducing ATG Portal: Closings Simplified

At Attorney’s Title Group, communication is one of our top priorities. Offering convenient closings is equally important. A few years ago, we implemented the use of CloseSimple as an enhanced method of communication with real estate agents, lenders, buyers, and sellers to keep everyone updated of each step of the closing process.

Now we’re taking it a step further to make things even easier for our customers. We’re excited to announce ATG Portal. In addition to sending buyers, sellers, real estate agents, and lenders proactive communication throughout the entire process, ATG Portal is a secure platform to see and share everything related to your closing. This includes updates at each milestone of the process, plus on-demand access to important closing documents.

The ATG Portal allows all parties to digitally interact with all of their transactions in one place and on any device. It is web-based, so it is easily accessed from a computer, smartphone, or tablet. More importantly, it’s secure.

With the ATG Portal, buyer/seller interviews can be completed quickly, documents can be reviewed in advance, wiring instructions can be verified, and documents can easily be reviewed after closing is complete.

more

Combating Seller Impersonation Fraud in Real Estate

Fraud in the real estate industry is constantly evolving. Scammers are continuously searching for vulnerabilities to exploit, putting buyers and sellers at risk. Lately there have been several alarming stories of in real estate fraud in the news, shedding light on the need for heightened vigilance.

Real Estate Fraud Tactics Evolving with Technology

From wire fraud to social engineering schemes, fraudsters have long targeted real estate transactions. One of the more common forms of wire fraud is when a scammer impersonates a title company or real estate agent to get a buyer to transfer funds into a fraudulent account. Recent advancements in technology, such as the use of generative AI, have added a new layer of complexity to these fraudulent activities. AI tools like chatGPT are being employed to mimic voices, enabling scammers to spoof phone numbers and execute more convincing social engineering tactics.

Generative AI has led to a rise in realistic-sounding voice messages and deceptive emails, making it increasingly difficult to distinguish between genuine communications and fraudulent attempts. Scammers use this technology to manipulate victims into transferring funds or disclosing sensitive information, exploiting the trust inherent in traditional communication channels.

more

Key Players in a Real Estate Transaction: How Collaboration Seals the Deal

Real estate transactions can be complex and intricate processes. Whether you're buying your dream home, selling a property, investing in real estate, refinancing your loan, or engaging in any type of real estate transaction, numerous key players are involved. These individuals or entities play a vital role in ensuring a successful and legally sound transaction. Let's dive into who these key players are and how they work together harmoniously to close the deal.

Buyers and Sellers

At the heart of every real estate transaction are the buyer and seller. The buyer is the party looking to acquire the property, while the seller wants to part with it. These two individuals or entities are the primary decision-makers in the deal. They negotiate the terms, agree on the purchase price, and ultimately decide whether to move forward with the transaction.

Real Estate Agents

Real estate agents act as intermediaries between the buyer and seller. They help market the property, find potential buyers, and facilitate property showings. For buyers, agents can assist in locating suitable properties and negotiating on their behalf. They know the market, they know how to negotiate, and they keep you informed every step of the way. Their expertise in the local real estate market is invaluable when buying and selling a home.

more

Should I Worry About an Easement on a Property I’m About to Buy?

You’re about to close on your dream home. Then you meet with the title company and learn that the title search discovered that the property is subject to an easement.

What is an easement?

An easement gives another party the right to access your property and to use it, or a part of it, in specified ways. An easement agreement between two parties outlines the specific use of the property, along with any applicable payment and termination information. These easements are usually transferred when the property is sold. Though they are not always common knowledge, easements are more common than some may think, and it’s important to be aware of what they are and how they work.

In essence, an easement is a grant of a nonpossessory property interest that gives the easement holder the right to use someone else’s land. This might be something like a utility company needing to come in and repair water or sewer lines or trim trees that impede power lines.

Sometimes, easements can be to the property owner’s benefit. Using the example above, you will want the local power company be able to access the power lines on your property to restore power in the event of an outage after a severe storm.

more

Robbie Wilson voted among Little Rock's Best Lawyers

Attorney's Title Group is proud to announce that Robbie Wilson was voted one of Little Rock's Best Lawyers in the December edition of Soiree magazine. Robbie was recognized in the Commercial Real Estate category.

The Little Rock Best Lawyer list is composed of 113 individuals who were determined via a two-component voting system of peer review voting and voting by the readers of Little Rock Soiree and Arkansas Business magazines. The expertise of lawyers is used to determine who should be on the list, and readers votes and experiences with the lawyers determine how individual lawyers rank.

Congratulations to Robbie on this well-deserved achievement.

more

When to Say “NO” to FSBO: Top Reasons to Use a Real Estate Agent to Buy or Sell a Home

Buying and selling a home will be the largest financial decisions many people will make, so thinking about how and when to save money on the purchase or sale of a home makes sense. Without knowing all of the details, it can seem like selling and buying a home on your own is the way to go. After all, why spend money on a commission for a real estate agent when you can DIY? While selling or buying a home on your own can seem tempting, using a real estate agent actually makes more sense, financially and logistically, when you start to consider the potential roadblocks of doing it on your own.

Lower Sales Price

Homes sold by owners without a real estate agent often sell for less. According to the National Association of Realtors, in 2022, the median home sale price for homes sold by owners was just $225,000 compared to a median price of $345,000 for agent-represented sales. A real estate agent has the knowledge and experience to price your home correctly, market it effectively, and for both buyers and sellers, negotiate the best possible deal. Something else to consider: If you do try to save money on a commission by selling or buying a home without professional help, you’ll be responsible for all the leg work (which is a lot). Remember the saying, “Time is money?” When selling your home without a qualified real estate professional, expect to spend dozens of hours showing your home (or arranging times to view homes if buying), collecting information and paperwork, learning the details needed to comply with the law, and ensuring you have everything you need to close.

more

Attorney's Title Group Northwest Arkansas Office Grand Opening

Attorney’s Title Group (“ATG”) previously announced its expansion into Northwest Arkansas and the hiring of Rick Long as the new Director of its Northwest Arkansas operations.

The firm has officially opened its doors in Rogers in the Village on the Creeks center. The address is 2102 S. 54th Street, Suite 2, Rogers, AR 72758. They are hosting an open house on Thursday, November 9th, from 11:00 AM-2:00 PM. Details can be found on the Attorney's Title Group Facebook page at the following link: https://fb.me/e/O6CRJRYF.

Attorney’s Title Group offers remote, concierge closings at real estate offices, banks, and businesses. Attorney’s Title Group welcomes all businesses and homeowners in the region to experience the “Attorney’s Title Group Difference.”

more

Fun with Real Estate Jargon - Grantor vs. Grantee

Buying a home or piece of property is a really big deal. Once you’ve found the perfect place, you start envisioning yourself in it. You think about where to place furniture and hang pictures. You may envision hosting guests, celebrating important milestones, and making memories in this special place. Buying real estate is a truly exciting experience.

Going Beyond the Exciting Part

While finding and falling in love with a property is exciting, there are some less-than-exciting parts of the process, too. This includes familiarizing yourself with some of the documents and terminology that you may come across on your real estate journey. Though understanding terms like “grantor” and “grantee” isn’t the fun part – and not always necessary when you’re working with a trusted real estate professional – knowing the details is helpful in fully understanding your real estate transaction.

In broad terms, a grantor is the individual who transfers ownership to another person or entity, and the grantee is an individual who receives the transfer of the property. To simplify it, in a real estate transaction, the grantor is the seller and the grantee is the buyer. While much of this is straightforward, the obligation for each party depends on the specific transaction. The grantor may be the seller of a home, the landlord of a rental property (lessor), or a borrower who gives the mortgage (mortgagor). The grantee is the buyer, the lessee in a rental transaction, or the lender/mortgagee.

more

Attorney’s Title Group Announces Expansion, New Director in Northwest Arkansas

LITTLE ROCK, AR (August 7, 2023) – Attorney’s Title Group (“ATG”) has announced that it is expanding into Northwest Arkansas and has hired Rick Long as the new Director of its Northwest Arkansas operations.

Long brings a wealth of experience to Attorney’s Title Group. His background in title, construction, and banking will be beneficial to the company as it expands into the Northwest Arkansas region.

“We are glad to welcome Rick into this new position, and we’re excited about what it means for the continued growth of ATG. Rick’s experience and knowledge of the industry will be a big asset as we expand our footprint,” said Robbie Wilson, co-managing partner of Attorney’s Title Group.

In addition to implementing ATG’s core policies of customer service, Long’s role as director will include managing Northwest Arkansas business development, conducting closings, and working with the ATG operations team to ensure that the client experience with Attorney’s Title Group is first rate.

“At Attorney’s Title Group, we’re always focused on providing the best white-glove experience possible,” said Jack Harvey, the firm’s director. “We are confident that Rick will help us continue to provide excellent customer service to the Northwest Arkansas community.”

more

AI and Real Estate Professionals

It can pass the bar exam, write your kid’s college essays, and have a close personal relationship with a New York Times journalist. Across industries, some are wondering if they can be replaced by AI. The real estate business is no exception.

What is AI?

Artificial intelligence (AI) creates mechanisms that can analyze and process data, find patterns, and make decisions based on what those mechanisms learn. While there is still much dispute about how close AI can come to simulating human intelligence, learning, and decision-making, it’s a rapidly evolving technology with the potential to upend how almost everything is bought and sold.

Faster, More Efficient

The upside of AI is, principally, speed. For buyers, sellers, and real estate professionals, it involves a quicker way to analyze market trends, see property listings in target markets, and get comparable prices. Real estate professionals can use the consolidation of vast amounts of data for marketing purposes, negotiating deals, and providing their clients with personalized advice.

more

Attorney’s Title Group Joins Little Rock Regional Chamber Talent Recruitment Campaign

LITTLE ROCK, AR (May 1, 2023) – Attorney’s Title Group is excited to announce our participation in the Little Rock Regional Chamber’s national talent recruitment campaign, Little Rock Love Connection. Inviting both former Arkansans and potential newcomers to love Little Rock, Attorney’s Title Group will be among the list of businesses eligible for customized job matching. Interested applicants can visit movetoLR.com to submit an application to be matched and qualify for a $10K signing bonus.

“Central Arkansas has so much to offer, which is why we’re committed to helping people call it home. We know that this campaign will help people discover the excellence of living and working in Little Rock,” said Robbie Wilson, Co-Managing Partner. “Whether you are a match for ATG or another partner in this campaign, we hope we can be a part of welcoming you back to Little Rock.”

Cash incentive-based talent recruitment campaigns are gaining popularity nationwide to bolster local workforces for expanding economies. The Little Rock Love Connection campaign takes a unique approach by inviting Arkansas natives, as well as newcomers, to “come home” while also allowing current residents to act as matchmakers and potentially earn $501 for every successful match.

more

Buying Property: What is Tenancy in Common?

Ownership of real property comes in a variety of forms, with the four most common types being:

- Sole ownership by a natural person or a limited liability company or corporation

- Tenancy by the entirety, which applies to ownership by a married couple. Upon the death of the spouse first to die, full ownership vests in the surviving spouse.

- Joint tenancy by two or more persons, which means each of the owners holds equal interests, all must receive their interest at the same time, and all must acquire their interest by the same deed. When one joint tenant dies, their interest transfers to the remaining owner(s). Upon the death of the last joint tenant, the property passes to that last tenant’s heirs.

- Tenancy in common, which can be equal or unequal ownership between two or more people. When one of the tenants in common dies, their share goes to their heirs.

What’s the Difference Between Joint Tenants and Tenants in Common?

The main difference between these two forms of shared ownership is that joint tenants have a right of survivorship, while tenants in common do not.

With joint tenancy, owners hold equal shares of a property with the same deed acquired at the same time. When one joint tenant dies, their interest passes to the remaining joint tenants. This is known as a right of survivorship. The marital rights of a spouse of a joint tenant do not attach to the joint tenant’s interest. At the death of the last surviving joint tenant, he or she can dispose of the property as they wish in their will.

more

What is a “Fixture” in Real Estate?

So you’ve fallen in love with a house—and its sparkling dining room chandelier. Is that chandelier yours when you close on the deal? It depends. On the other hand, if you are the seller and want to hold onto the sparkling chandelier, there are some important things to consider.

Fixtures: A Brief Definition

A fixture is personal property attached to real estate property. While the definition varies from state to state and should be addressed in a purchase agreement, if the object needs nails, screws, bolts, glue, pipes, or cement to install in the home, it is usually considered a fixture, which means it conveys with the sale.

Determining What is a Fixture and What Isn’t

Something like a curtain rod purchased by the homeowner may be personal property at first, but once it is affixed to the wall, it becomes a fixture of the home. There are several grounds for determining what can be considered as real property (items attached to the property) versus personal property (sometimes called “chattel”). Sometimes a real estate agent may use a process called “MARIA” to help a homeowner determine what can stay and what can go. Below are some of those guidelines:

more

What to Know Before You Invest in Out-of-State Real Estate

Investing in out-of-state property appeals to people for a variety of reasons. If you live in a market with stratospheric housing prices, it’s likely crossed your mind to invest in a lower-cost area. Or maybe you want a place for your college-age child and roommates who can subsidize a mortgage with rental payments, or a vacation home to enjoy or rent out when you’re not there.

An important consideration when investing in real estate is the return on investment (ROI). For many people thinking about markets outside their own, factors like lower purchase prices, reduced property taxes, housing regulations favorable to rentals, and potential appreciation rates can lead to a great return. While out-of-state investing may be appealing, it also comes with challenges.

It’s always a good idea to look before you leap. Below are some caveats.

Get to know the market intimately. In your own neighborhood, you likely know where the best shopping and school districts are located—and which areas are less desirable. This is not always the case in an unfamiliar area. Familiarize yourself with the area in which you plan to purchase property.

more

What is Title Insurance and Why Do I Need It?

In the transfer of real property, title insurance is a way to protect buyers and lenders from losses or damages as a result of liens, encumbrances, or defects in the chain of title or ownership. There are two types of title insurance: owner’s title insurance and lender’s title insurance.

The cost associated, also known as the premium, is paid on a one-time basis, typically at closing. The amount of insurance under an owner’s title policy will be the purchase price paid by the buyer. The amount of insurance under a lender’s title policy will be the amount of the buyer’s mortgage.

A seller’s clear title—or an understanding of why the title is not clear—is necessary to close any real estate transaction. The title company will do a deep search of the title records to uncover anything that might prevent the buyer from receiving a clear title. If title defects or clouds on the title are found, the title company will require documentation be filed in the title records to remove the defect or cloud.

Title insurance is a valuable tool because it results in greater protection of what is likely the single largest investment someone will make in their lives.

more

Funds Disbursement FAQs

You’re excited about the purchase of a new home. Congratulations! To make it happen, you’ll need the help of an experienced closing agent at a reputable title company in the critical step of funding the loan and tying up loose ends. The title company will oversee the closing process and make sure everything happens in the right order at the right time. The following are a few frequently asked questions.

What exactly is “funds disbursement”?

Receiving and disbursing funds for the sale is a key component of the settlement and closing process. The closing agent at a title company will work with the lender and/or you, the buyer, to facilitate the funds disbursement process. The title company where you’ll be closing will need a few things before they can assist you in closing on your house.

What does the title company need in order to close?

A title company must have approval from the lender to get to closing. The title company also needs lenders’ funds and funds from you, if applicable. If you are using a lender, your lender will provide your final cash to close amount. If it is a cash purchase, the title company will work with you prior to closing regarding the funds needed. These funds will go into an escrow account overseen by the title company.

more

Attorney’s Title Group, PLLC Announces New Location in Conway

Attorney’s Title Group (“ATG”), a real estate title and closing company based in Little Rock, has announced the opening of their new office in Conway later this month. The new location, at 685 Shelby Trail, Suite 102, will be the company’s second office in Arkansas, and will be managed by Lisa Fields, a closing agent who currently works in the Little Rock office. Lisa has a strong background in real estate and title, including 10 years of experience as a landman in addition to positions at mortgage banking and title companies.

“This has been a dream of mine for quite some time. I am super excited to bring ATG’s amazing real estate services to my friends and neighbors in the Conway community that I know and love so much,” said Lisa Fields.

Attorney’s Title Group provides residential and commercial title and closing services, real estate refinances, title insurance, title curative legal work, document preparation and review, REO services, and 1031 qualified intermediary services. The company focuses on providing their customers with personalized, concierge-style “white-glove” service and high-touch communication.

more

Tips for Selling A Home Faster

If you’ve decided to sell your house and move to a new place, you probably don’t want to sit around for months on end waiting for your house to sell. Preparing your home so it feels welcoming and fresh to prospective buyers is one of the best ways to sell it faster, no matter the market.

Upgrades

If you’re able to afford upgrades, spend your money wisely. For example, some potential buyers might avoid a pool or a newly added sunroom because these things can mean additional costs and ongoing maintenance.

On the other hand, most buyers will appreciate energy-efficient improvements or updated kitchen appliances and counters. Fresh, neutral-colored paint and flooring also help. Potential buyers will be checking out the attic and basement, so if those or any other stairways don’t have handrails, it’s worth adding them—they’re a practical upgrade, and they’ll help protect you in case of a stumble.

Put Your Home’s Best Foot Forward

Potential buyers want to envision themselves living in the new space, and they want to see a better version of themselves there: more organized, more relaxed, happier. Encourage them by making sure your home is neat, in good repair, and ready for them to envision it with their own tastes and personality.

more

Attorney’s Title Group Names Robbie Wilson as Co-Managing Partner

Little Rock, AR (August 24, 2022) – Attorney’s Title Group, an affiliate of The Wilson Law Group, is pleased to announce that Robert M. Wilson, III has been named Co-Managing Partner of Attorney’s Title Group. Robert (Robbie) M. Wilson, III currently serves as partner at Wilson & Associates and Supervising Attorney of Attorney’s Title Group. He will be co-managing with the current Managing Partner of Attorney’s Title Group, Jennifer Wilson-Harvey.

“Robert has shown an amazing ability to develop businesses and influence people. The culture he has helped establish at Attorney's Title Group is inspiring, and I am very proud of his accomplishments, both personal and professional. He is the right person to lead the firm into the future," said Jennifer Wilson-Harvey, CEO and Managing Partner of the firm.

Robbie received his education from Tulane University (B.A. 2009) and the University of Arkansas School of Law (J.D. 2013). He is licensed to practice law in Arkansas, Tennessee, and Mississippi, and is also licensed to practice before the 8th Circuit Court of the United States. He serves as the central Arkansas representative of the Arkansas Bar Association Young Lawyers Section, is a fellow of the Arkansas Bar Foundation, is a board member of the Pulaski County Bar Foundation, and is a member of multiple state, local, and national legal, banking, and real estate associations. Robbie was named partner of the firm in 2019 and serves on the firm’s Executive Committee. Robbie’s dedication and vision for both Wilson & Associates and Attorney’s Title Group has resulted in substantial business growth across the Wilson Law Group. He continues to grow Attorney’s Title Group within the real estate industry and as a pillar of the local community; notably, his leadership has led to the implementation of community-oriented programs which reduce closing fees for veterans, first responders, and teachers.

more

Want to Increase Your Home’s Value? Upgrade Its Energy Options!

Did you know that eco-friendly energy upgrades can make your home more sellable? According to a National Association of Home Builders (NAHB) survey, 57% of buyers will pay up to $5,000 more to save money on utilities – and energy upgrades are a key way to reduce those bills. To help you increase your home’s sale value, here are five energy upgrades to consider.

1. Install Energy-Efficient Appliances

Out of over 200 features listed in the NAHB study, 81% of respondents listed ENERGY STAR rated appliances as either non-negotiable or highly desirable. For sellers, one fairly cost-effective way to improve your home’s value – and increase its energy efficiency – is to switch out old, less efficient appliances like dryers and refrigerators for newer models.

2. Change to a Tankless Water Heater

Tankless water heaters offer two benefits: they take up less space than conventional systems, and they’re more efficient. Both advantages will appeal to buyers, thereby increasing your home’s value over time.

more

Wire Fraud – What it is and How to Avoid it

Email spoofing and wire fraud has been in the news again lately, so we're re-visiting one of our older blog posts to share some information on the subject.

In this article we’ll discuss some best practices to avoid being scammed when dealing with real estate transactions.

Good Funds

As real estate agents know, wiring is a common practice in real estate transactions. For those new to the industry, wiring money is one of a few ways to pay with “good funds,” or immediately available money. Other examples of good funds are cashiers’ checks, certified checks, and anything that is immediately collected. The idea is that no one wants to wait three days for a real estate closing, and a lot can go wrong in that time.

Spoofing Real Estate Professionals’ Emails

If you haven’t heard the term “spoofing,” it’s time to learn. Fraudsters find ways to forge emails with the name of a trusted person in the “from” column, and the contents of the email usually have detailed instructions for wiring a large amount of money. Usually these “spoofed” email addresses are “from” various people in a current real estate transaction, and generally at a key point in the process where funds will change hands. We have even heard of people trying to intercept the selling company, spoofing the seller’s email, convincing the title company to wire out the seller’s money to the wrong place.

more

Considerations When Buying New Construction

Ah, the smell of fresh-cut lumber. The notion that you, and only you, will be the first person to live in a house. For many, buying new construction is much more appealing than inheriting someone else’s taste in bathroom tile and paint colors, never mind aging plumbing or an old roof.

Buying a house always comes with some level of risk, and for many, the prospect of a shiny new home seems like a safer bet than a fixer-upper. But before you make a builder your new best friend, there are some things to consider.

Look at the Neighborhood

What are you looking for in a community? While you may fall in love with your dream kitchen, how will you fit in? If you are empty-nesters, for example, you may not relish the noise and excitement of young families. If you do have young children, you’ll want to make sure you are close to their activities, or you’ll find yourself constantly on the road for soccer practices and dance recitals.

If you’re comfortable doing so, knock on a few doors and ask how people like living there, and look at how the homes on the street appear to be holding up, especially those that are a few years old.

Consider Your Timeline

more

Beyond the Backsplash: What to Look for When Buying a "Flipped" House

It’s a real estate fairytale: What looks like a teardown is coaxed back into beauty by gifted contractors and designers. In the space of 30 minutes of viewing, we witness a transformation and a happy ending for the renovators and the new homeowners.

Over the past decade, we’ve seen TV shows and real-life examples of houses that have been remade, sometimes with more speed than seems believable.

If you’re in the market for a new home but have no DIY talent or interest in renovating, a property that’s already been updated can be very appealing. That said, how can you make sure it’s not just a quick spackle-and-paint job but actually a real value?

Here are some critical things to consider:

Water, water. Kitchens and bathrooms are well-known to be the biggest costs when it comes to renovations. Turn on all the faucets and look at how they well they work in terms of water pressure and temperature. Smell the water and look at the color. (Note: Brown is not good.)

Find the hot water heater. Is it new, a couple of years old, or ready for the Smithsonian? A replacement can be an expensive fix if you don’t plan for it. Look at the pipes around the heater and others that are exposed elsewhere in the house. Ensure they are newly replaced.

more

Doing a Real Estate Deal with Friends

Buying or selling a home—a large investment for many people —is a decision that demands real estate expertise. The first phone call many people make is to a real estate agent who is also a friend.

While it seems like a good idea in the first place, engaging in a real estate deal with a close friend can also present risks to both parties and to the relationship.

Downsides for Agents

First, consider some of the potential negatives when representing a friend.

- Personality conflicts. It’s entirely possible to enjoy someone’s company at a dinner party and yet still not mesh well in something as critical as a real estate transaction. Think carefully about whether this person will cede control to your professional expertise, or if they will second guess you at every turn.

- Higher expectations. A friend may assume that you’ll go the extra mile for them—and chances are you will—but late-night phone calls and constant texts may be more than your friendship can support.

- Constructive criticism may not fly. Your friend may not appreciate hearing that their barking dog or clutter level are putting buyers off, or that their wish list for a home in their price range is unreasonable.

Reasons Why Real Estate Deals Go South at the Last Minute (and How to Avoid Them)

Anybody who’s been through the sale or purchase of a home knows that “under contract” is just that: It doesn’t mean a deal is done. Seasoned real estate professionals can tell you there are common reasons why transactions get called off at the eleventh hour.

Getting a Good Real Estate Agent is Key

Avoiding the majority of last-minute house heartbreak can boil down to having an experienced real estate professional involved. They will:

· Negotiate on their party’s behalf throughout the transaction

· Confirm bank appraisal results

· Work with the home buyer (if applicable) on getting approval for a mortgage, if needed

· Follow up with attorneys as they review/prepare key documents

Now, on to the potential pitfalls that can keep a house from changing hands.

Inspection Issues

Inspections are a part of due diligence for both sellers and buyers; both must act in good faith to avoid nixing a deal. If you’re a seller, it’s key to hire a reputable home inspector who will produce a solid report so you can be upfront and avoid surprises for a buyer.

If you are a buyer, get your own inspection and look for red flags, including but not limited to: mold, pest infestations, foundation and structural issues, and roof leaks or damage.

more

DOs and DONTs for Fixing Up Your Home Before Selling

Have you decided to sell your home? Now you’ve got another important choice to make: which renovations or repairs to undertake before putting the house on the market. Keep these considerations in mind as you make your list of pre-listing “DOs” and “DON’Ts.”

First Things First: Factors to Consider

There are few, if any, absolutes about fixing up a home for sale. Before you even contemplate a kitchen upgrade or a paint job, do your homework and get your real estate agent’s input on these crucial considerations:

● The Overall State of the Market. Whether it’s a buyer’s or a seller’s market will greatly influence how quickly your home may sell, and for how much, with or without improvements.

● The Look of Local Competition. A Comparative Market Analysis can tell you the value of recently sold similar homes in your area and help you crunch the numbers on renovations. It’s also smart to attend nearby open houses to scope out the competition for yourself.

more

Introducing Lisa Fields: Closing Agent

Attorney’s Title Group is excited to announce our newest closing agent, Lisa Fields. Lisa was previously serving as closing assistant before accepting the position as closing agent. Lisa has a strong background in real estate and title. She worked as a landman for 10 years completing title work, curative, leasing, and due diligence for several petroleum exploration companies for the purposes of oil and gas exploration in Arkansas. When those companies exited the state, she then worked in various positions at mortgage banking and title companies, applying the knowledge and skills learned from her experience as a landman. Prior to joining Attorney’s Title Group in May of 2020, Lisa worked for three years in the Title Curative department of Wilson & Associates.

Check out this brief Q&A with Lisa to get to know her better:

Q: What was the best vacation you have ever taken and why?

A: The best vacation I have ever taken was with my family and our close friends to the South Rim of the Grand Canyon. I can still close my eyes and remember how beautiful and surreal the views were, absolutely breathtaking! The annual stargazing party just happened to be taking place one of the nights we were there. Hundreds of telescopes set up looking up at the clear night sky. I could see the rings on Saturn!

more

Winter Home Maintenance Tips

The weather in Arkansas can be unpredictable. When it comes to winter, there is always some chance of experiencing 65-degree temperatures and snow in the same week. To be on the safe side, it’s a good idea to take advantage of the warmer temps to prepare your home for the possibility of winter weather. The following tips will help prepare your home for warmth and safety during the colder months.

Indoors

Seal any cracks and openings. Drafts through windows and doors can cause heat loss and increase your energy bills. Feel around doors and windows for air leaks (or use a candle) to determine if there are any openings where heat can escape and cold air can enter. Add caulk or weather-stripping around the openings. Use heavy-duty plastic or a window insulator kit to further seal windows. It’s also helpful to cover other openings to your home, like pet doors.

Reverse ceiling fan blades. In the warmer months, ceiling fans rotate counterclockwise. Use the sliding button (near the fan blades) to switch the blade rotation of your ceiling fan so that they rotate clockwise to push the warm air down from the ceiling.

Cover bare floors. Hardwood, tile, and laminate flooring can cause your house to lose heat, not to mention cause cold feet! If you don’t have carpet, consider adding rugs over areas with bare flooring to keep your floors and feet warm.

more

Spruce up or Sell? What to Fix and What to Forget When Selling an Older Home

Marketing a home with a few good years (and not a lot of maintenance) on it can be daunting. While some buyers are great at seeing potential, some lack vision—seeing past the pink bathroom tile or dated floral wallpaper, for example, can be a real stretch for the non-designers among us.

A home that needs repairs may take longer to sell than one that has been well-maintained. But major upgrades can run into tens of thousands of dollars. So, with a given property, how do you decide between selling it as-is or investing in fixes? There are a few key questions to ask.

Who’s your buyer (and where)? Again, while there are a special few who can see the charm and potential in an older home, most can’t envision how an outdated space could work once it has been updated.

Much depends on the neighborhood. Is there a preponderance of teardowns followed by new builds? If so, the land represents the real value, and work on the property isn’t always necessary to generate a return on the investment. If it’s an area where older homes are routinely rehabbed, some judicious changes could bring a higher yield from the market.

Finally, if a turnkey buyer is your target—and an actual possibility—then you’ll be looking for a general contractor and looking at months on the project and, to do it properly, a significant financial outlay.

more

Selling a "Haunted House"? Here's What You Should Know

With the spooky season approaching, it seems like a good time to revisit the “haunted house” statute. A question that agents have asked in the past: Do I have to tell a potential buyer that a property might be a “haunted house”?

In 2009, this was a legal gray area. Does the Realtor owe a duty to the buyer to make an inquiry about past events in the house? Can a buyer sue a Realtor for psychological damages if past events weren’t disclosed and the buyer claims the house is haunted?

The answer to both questions, as of 2010, is “no." In 2010, the legislature definitively passed Statute 17-10-101, otherwise known in the industry as the “Haunted House Statute.” This statute defines houses as psychologically impacted if there was a homicide, suicide or felony on the property. It further states that this is not a material fact of information to disclose during a real property transaction, and that a Realtor cannot be sued as a result of not disclosing, inquiring, or releasing information if a property is psychologically impacted.

What it means for the buyer: Since this information is not legally available from the agents, there are a few alternative paths if this would impact your purchase:

more

The Logistics of Buying and Selling a House at the Same Time

Are you considering selling your home and buying a new home? If so, you have two options: sell your current home before buying a new one or buy a new home before selling your current home. This can be a complicated decision. Whichever way you choose to proceed, you will want to have a solid plan and steady cash flow to keep the conveyancing process running smoothly. The first thing you should do is reach out to your real estate agent and lender to discuss your options, as they’ll be able to work with you on strategy and timing. Beyond that, the following are a few considerations when buying and selling a home simultaneously.

Selling Your House Before You Buy

From a cash flow perspective, it is more convenient to sell a house before you buy another property. Not only will you know exactly how much you can afford to spend on a new home, but also you will already have the funds available to close.

Choose your settlement date wisely. Ideally, you should settle and close your new property on the same day. If this is not possible, be sure to plan in advance where you’ll stay until you can move into your new home. You might:

- Opt for a short-term rental

- Stay with friends or family

- Ask your buyer if there is any flexibility – would they be willing to negotiate the settlement date?

Real Estate Contracts and the Force Majeure Clause

The real estate market is booming right now. Sellers are scrambling to get their properties on the market while buyers face fierce competition, often resorting to cash offers over the asking price. The result is often a lightning-fast round of negotiation in hopes of winning the contract. Unfortunately, in the haste to secure the deal, it can be easy for sellers and buyers to lose focus of how important their real estate contract terms are.

All real estate contracts must be in writing and contain certain provisions, including:

- An identifying description of the parties

- A legal description of the property

- The purchase price of the property

- Legal consideration and mutual assent

In addition to the terms listed above, many real estate contracts contain a force majeure provision. The force majeure clause protects parties who cannot perform their contractual obligations due to circumstances beyond their control. Often, circumstances that invoke force majeure are labor strikes, raw materials shortages, riots, natural disasters, and “acts of God.”

more

Discovery of Damage After Closing: What Should You Do Next?

After all of the work involved with house hunting, inspections, packing, and preparing to move, closing on your new home should be something to celebrate! But discovering major problems with your home after closing can cause a major headache. While maintenance is an expected part of homeownership, the presence of significant damage or environmental concerns might have caused you to rethink purchasing the property in the first place.

What Types of Hidden Damage Could You Find?

Most home inspections can uncover hidden issues before closing, such as an unstable foundation or water damage. However, inexperienced or unqualified inspectors can potentially overlook major problems, which can leave you with expensive home repairs on your hands after you’ve just been handed the keys. Some of the most common types of damage that may be missed at inspection (or due to lack of inspection) include roof leaks, defective appliances, faulty heating or air conditioning units, and flooring issues.

Additionally, environmental pollutants are not only costly to remedy but can cause health problems for you and your family. Some of the most common types of environmental threats in a household include mold, lead paint, carbon monoxide, radon, pesticides, and volatile organic compounds. Indoor air quality is a huge threat to your family’s well-being, so obviously, these types of problems will need to be addressed immediately.

more

Not All Home Renovations Add Resale Value

When we purchase a home, we want to make it a comfortable and unique space for our family to live – but it’s important to remember that a home is also an investment. When making improvements to your property, take a moment to consider whether each project will help add value to your home in the long run. If you’re planning to sell your home one day, the following types of renovations might do more harm than good.

- DIY home improvement projects: After streaming hours of HGTV during the pandemic, it can be easy to assume anyone with a hammer and an idea can renovate their home. While some projects can be tackled by a first-timer, some bigger renovations may need the help of a professional. You may feel satisfied with your handiwork, but potential buyers and home inspectors can usually spot shoddy or unskilled workmanship. Before embarking on a DIY project, It’s important to do a little research first.

- Converting the garage into living space: Especially for growing families in older or smaller homes, it can be tempting to maximize your space to lounge and play – and one of the most obvious places to start is the garage. While converting an existing garage space might initially seem like the best idea, many homebuyers may have opposite preferences and would choose a home with a garage to a larger living area. Again, this is something you should research and then evaluate the pros and cons before making your final decision.

- Unusual wallpaper, lavish light fixtures, or other highly personal touches: Sure, you might love jungle-themed or brightly colored floral wallpaper, but think twice before using it to cover your whole bedroom. Even with wallpaper becoming more popular again, wild and quirky patterns are only likely to appeal to a select few, and can potentially make your home harder to sell. The same goes for trendy light fixtures that quickly go out of style, as well as other fixtures and materials that seem exciting in the moment. It’s important to make your house uniquely “you” but for more permanent fixtures, also consider what would appeal more universally to buyers in the future.

- A high-end kitchen: While a newly remodeled, up-to-date kitchen is a boon for the value of any home, it is possible to overdo it when doing a major kitchen remodel and selecting only the most high-end options. On average, a complete high-end kitchen remodel costs more than $60,000 but has a resale value of about $20,000 less, meaning you won’t come close to recouping your costs. Instead, turn your focus only toward replacing the items that really need it, and go for mid-range appliances and fixtures instead of the top-of-the-line stuff.

Introducing CloseSimple: The Pizza Tracker for Title

At Attorney's Title Group, communication is important to us. Part of our concierge-style service is to ensure all parties involved in the closing process receive direct, reliable communication. We're excited to now be able to provide even better communication with the technology we've recently implemented.

If you’ve ever ordered a pizza from Domino’s you know all about their Pizza Tracker and how it helps customers know where their pizza is at as it’s being made. You can track everything from when the dough is being tossed, when the toppings are added to when the pizza enters the oven, and as it leaves for delivery. If you can track the status of your pizza, you should be able to track the closing process.

After months of hard work, we have recently unveiled CloseSimple, a way to help us communicate with agents, buyers/sellers, and everyone else involved in the closing process with a visual Pizza Tracker for Title™.

We’ll also be able to send short text messages to agents to notify them of completion along the way (since we know a text is often easier to read than an email).

We're looking forward to using CloseSimple on your closing! Please contact us if you have any questions.

more

If You Have Children, Consider These Things When Buying a Home

Buying a home can be an exciting time of change and opportunity for a family, but when you have kids, this can add a layer of complexity to the process. Not only do you have to account for the needs and desires of the adults in the household, but certain considerations must be made for the happiness and well-being of the children as well. This may ultimately impact the size and location of the home you choose to buy. Here are a few important factors to consider.

Research the Quality of Area Schools

Perhaps the most important factor to mull over when buying a home with kids is where they will be attending school. Is the home located within the boundaries of your preferred school district? This is important not only for your children’s education, but it can help you sell your house later as well. Data shows homes in high-performing school districts typically sell faster and go for a higher price. To simplify the process of searching for a home, it might be helpful to determine the boundaries of your desired school district before you begin narrowing down your favorites.

Pay Attention to the Home’s Size and Floor Plan

Make sure your future home is the right size for work, play, relaxation, and storage. Is the kitchen big enough for family meals? Are there enough bathrooms to avoid feeling overcrowded? Particularly if your family is still growing, it may be wise to choose a bigger home that will allow everyone to have the breathing space they need. When looking at the home’s layout, you may also wish to consider whether you will want certain rooms to serve different functions – for instance, it would not be ideal for the home office to be directly adjacent to the children’s play area.

more

Technology & Real Estate

Over the last 10 years, technology has transformed and bolstered the real estate industry, making transactions more efficient and convenient for agents and homebuyers alike. Technological advances such as electronic signatures, virtual home tours, and online home listings have become so ubiquitous that they now seem almost essential for any potential homebuyer – but looking to the future, there are still many exciting ways technology can continue to empower the real estate sector over the next decade.

Consumers Want Seamless Online Sales

The development of secure financial digital tools has allowed easy data access and transfer, making it possible to move home sales entirely online. As this technology becomes faster, safer, and less expensive, asset transfers that occur in a completely virtual environment are likely to become more common. Additionally, notarization has also started to migrate online due largely to the development of more secure programs. As the rest of the home-buying process goes virtual, it makes sense that over the next 10 years, notarization and other transactional aspects will follow.

more

Due Diligence Steps When Buying New Property

Purchasing a home or another piece of property is an expensive and often life-changing decision that should not be taken lightly. Before making such a major purchase, it is essential that you perform due diligence, which simply means you are being responsible and doing your research on the property prior to signing any documents or contracts. That way, you have full knowledge of any issues that may arise, and you can feel good about your investment.

Regarding real estate, performing due diligence includes several primary duties. A few of the basic items include:

- Know the market: Before you purchase a home, get to know the neighborhood and the typical value of the surrounding homes. Talking to residents can help you learn more about the area. It’s best not to rush into a decision.

- Get an inspection and appraisal: An appraisal determines a property’s value, and different types of inspections can help spot problems with plumbing, electrical, the roof, appliances, the foundation, drywall, and many other vital things. Inspectors also look for threats such as wood-destroying organisms, lead-based paint, and radon gas. Knowing a property’s true value – as well as any major repairs it may require (or risks it might create) – can help you make an informed decision about your purchase.

- Find the best deal for financing: Many buyers don’t take the time to get several bids for mortgage financing, but doing so could help you get a better deal and save you thousands of dollars in the long run.

- Find out what kind of insurance you’ll need: Homeowner’s insurance is a must – it will cover losses from natural disasters, theft, fire, and other causes. However, some homes are costly to insure due to their location in an area where flooding, earthquakes, or tornadoes are common – and in some cases, certain properties cannot be insured at all. Before buying a home, find out how much insurance will cost, and shop around to see who can offer you the best price.

Has the COVID-19 Pandemic Changed What We Want in a Home?

In home design trends, as in life, sometimes it feels like change is the only constant. While only a year ago, breezy living rooms and kitchens that promote family togetherness were all the rage among homebuyers, the COVID-19 pandemic has prompted many people to reconsider what they desire in their dwelling.

For starters, we’re all spending a lot more time at home these days – probably a little more than we’d like, as many jobs, schools, and activities shift to a virtual environment. Our lives will probably look this way for a while, so it should come as no surprise that homebuilders and real estate agents are beginning to consider how our homes can accommodate our changing way of life.

One key feature that’s seeing a decline in popularity is the open floor plan. Homebuyers are again starting to favor walls and doors between rooms that allow each family member to work, study, and live in their own space. In this same vein, home offices have become more desirable – and it’s likely a bonus if these dedicated workspaces are equipped with noise control. Separate spaces to keep kids occupied while parents work are also in demand, along with home gyms and breakfast nooks.

more

Home Upgrades to Consider When Selling

If there’s any insight to gain from 2020, it’s this: the home buying market is resilient. Despite the fact that home buying slowed earlier in the year, the market has started to rebound. This rebound is partly due to low mortgage interest rates allowing first-time homebuyers to purchase when they may not have been able to before the pandemic. Another driving force behind the rebound: millennial homebuyers. In 2019, millennials made up 38% of homebuyers.

Regardless of the buyer’s generation, these are some of the upgrades and trends a buyer may be looking for in the search for their next home.

Smart Home Features

There used to be a time when smart home features were out of reach for some people, but now, with companies like Amazon, Google, and Ring, smart home features are more affordable. Tech savvy or not, some homebuyers are more interested in homes with smart home security, smart thermostats, smart speakers, and smart lighting upgrades that can be controlled from a cell phone.

more

We're Moving to a New Location!

Attorney's Title Group is excited to announce that we are moving to a new location. Beginning November 1st, we will be in our new location at 5315 Highland Drive. The new location provides us with more space and added convenience to better serve our valued clients.

It’s true that 2020 has brought a lot of change to our lives, but we think this will be a good change. Our address is changing, but our phone number, email address, website, and excellent customer service remain the same.

We hope you’ll drop by soon to see our new space.

more

How “Virtual” Options are Helping Buyers and Sellers during the Pandemic

For sellers, an “open house” means more visibility since buyers can swing by and view the home without making an appointment. An open house can be a fantastic way to have multiple home showings in a condensed period of time. Like many other things complicated by COVID-19, the pandemic poses another problem for realtors: Open houses may not always be feasible for some prospective homebuyers. With stay-at-home orders being passed in many states, in-person showings and open houses were down as much as 40%-50% in April.

As Americans are getting back to work, buyers and sellers are returning to the market. While open houses are starting to get going again, some realtors are relying on technology to conduct digital home walkthroughs, virtual open houses, and even “virtual staging.”

Digital Walkthroughs and Virtual Staging

Virtual staging is the use of software to add digital enhancements like furniture and other furnishings to the image of a property. Instead of temporarily bringing in furniture and other decor to make a home appear more attractive to potential buyers, some realtors are using digital technology to the same end. This saves realtors and sellers money on purchasing or renting furniture and moving it in and out, all while limiting the amount of person-to-person contact involved.

more

Bills of Assurance: The Basics

Residential communities with a governing document (such as a bill of assurance or declaration of covenants, conditions and restrictions) foster a cohesive, clean, neighborhood atmosphere. They spare property owners some responsibilities while also requiring those property owners to follow certain rules and regulations. A BOA will have its own set of rules, regulations and procedures. The BOA can help you better understand your role and responsibilities as a homeowner in your community.